2 min read –

Aluminium is silently shifting from Gulf to ASEAN –

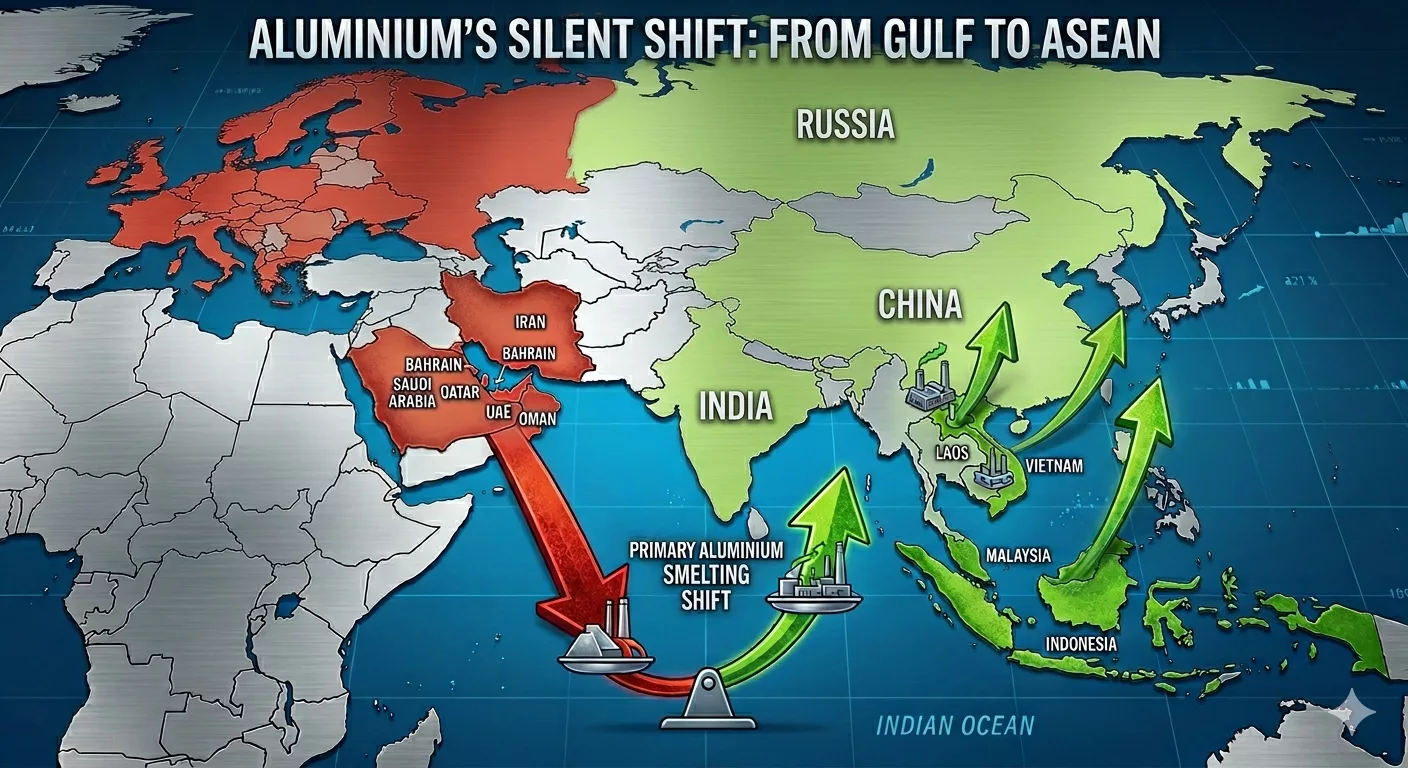

6 million tons under threat in the Middle East –

5–6 million tons rising in ASEAN by 2029 –

The global map of primary aluminum smelting is being redrawn as we speak.

The ongoing USA-Israel-Iran war in the Middle East is speeding up a redistribution that was already underway.

In 2025, the Gulf smelters (UAE, Bahrain, Saudi Arabia, Qatar, Oman) produced around 6 million metric tons of primary aluminum, roughly 9% of world output.

Iran adds another ~500,000 tons, mainly from SALCO, IRALCO, and Almahdi.

Yet the conflict has already taken a toll: two Gulf smelters (EGA Al Taweelah, Alba) have been directly hit, threatening 3 mtpa (million tons per annum) which is half of the region’s capacity.

At the same time, Western & Central Europe continues its long-term decline. High energy costs and two decades of deindustrialization have led to repeated smelter curtailments and closures.

Recent examples include the full shutdown of Slovalco in Slovakia (2022) and Alcoa’s San Ciprián smelter in Spain (curtailed since 2021).

Meanwhile, Southeast Asia is seizing the moment.

In early Feb 2026, Laos announced a new 1-million-ton-per-year smelter, with first metal expected in 2028/2029.

Indonesia revealed plans for “INALUM 2”, a 600,000-ton facility on the same timeline.

Vietnam’s THQ smelter in Dak Nong is set to produce its first aluminum in Q2 2026, at 450,000 tons of capacity.

ASEAN currently accounts for about 1.5 million tons (2% of global production), led by Press Metal in Malaysia (1 million tons) and Indonesia’s existing INALUM 1 (300,000 tons).

Once the new projects ramp up fully, including others such as Adaro and Tsingshan in Indonesia, the region will reach 5–6 million tons annually, tripling today’s output.

For context, here’s the 2025 global picture:

(million tons per annum = mtpa)

• China 60% 44 mtpa

• Middle East 9% 6 mtpa

• India 5% 4 mpta

• Russia 5% 4 mtpa

• USA+Canada 5% 4 mtpa

• Europe 4% 3 mtpa

• Oceania 2.5% 2 mtpa

The tragic human and economic cost of the on-going Middle East war is undeniable.

Yet it is also accelerating a broader shift: the center of gravity of the global economy is moving eastward.

New capacity is rising where energy is more secure and investment is flowing.

The West feels increasingly unstable; the East increasingly reliable.

People and markets prioritize stability and prosperity.

Political regimes seem to matter less than they once did.

What do you think?

Is this the new normal for strategic metals?

Throw your thoughts at bonjour@cintasia.com or on LinkedIn (link below).

We are CINTASIA, we help you develop your sales and operations successfully in Indonesia.

We specialize in technology and industrial equipment.

PS: To know more about the aluminum smelting process, click here

https://lnkd.in/gx__WKbB

Picture : Gemini

Source: CintaGrok